The Future of the Renminbi as an International Currency

China is successfully promoting the use of its currency, the renminbi (RMB), for international trade and investment. Economic logic suggests that this will eventually require full convertibility—the ability to change the RMB into another currency for any purpose and in any amount, without restriction. RMB reserve currency status1 will also require China to establish an open capital account and deeper and more competitive capital markets.

Thus, although internationalization of the RMB has attractions for both China and the rest of the world, it presents substantial challenges. In the short term, China’s highly controlled exchange rate, capital account regime, and structural current account surplus complicate efforts to generate outflows of RMB and manage return inflows of RMB. Its relatively high inflation also makes the authorities reluctant to facilitate returning RMB.

In the longer term, opening the capital account would force China to make its exchange rate more flexible in order to retain control over domestic interest rates. Given the reduced role this would imply for the government in the economy, political considerations may block complete convertibility for investment purposes for many years to come.

Why Internationalize?

In 1993, China indicated that it was committed to achieving full currency convertibility by the end of the century. It began removing capital account restrictions gradually and established current account convertibility in November 1996. When the Asian financial crisis erupted the following year, however, China dropped its full-convertibility target.2 And, while senior financial officials still maintain full convertibility as an objective in private discussions, the government no longer provides official commitments or timetables.

Nevertheless, since late 2008, China has accelerated efforts to promote the RMB as an international currency. Why?

A primary motivation is to reduce its dependence on the dollar. Public opinion—pushed by a recent Chinese bestseller, Currency Wars, to believe that the United States is seeking to reduce its debt burden by depressing the value of the dollar—is concerned about the value of China’s ample dollar reserves.3 Meanwhile, authorities worry that China’s reliance on the dollar4 for invoicing and settling trade can hurt exports.5 After Lehman Brothers collapsed in 2008, Chinese exports plummeted—not only because final demand fell, but also because credit froze in many importing countries, limiting importers’ access to trade financing.

Turning the RMB into a trade settlement currency will reduce the risk of such shocks to China. It will also better protect Chinese exporters from currency risk and reduce or eliminate costs associated with hedging against that risk. Similarly, using the RMB as an investment currency will help eliminate exchange rate risk for Chinese firms seeking to borrow money for international investment. In addition, increasing RMB use should, over time, help lower China’s excessive foreign exchange reserves.6

Implementation in the Short Run

Following the global financial crisis, China worked to better protect itself by intensifying efforts to internationalize the RMB and to develop an offshore market for the RMB. However, the country’s capital account restrictions, current account surplus, and high growth have complicated attempts to get foreigners to hold large amounts of RMB outside of China; traders want to use their RMB to buy Chinese goods and investors want to invest their RMB in Chinese assets. In fact, given these pressures, without the widespread expectation of further RMB appreciation, China’s push to create an offshore RMB market would have been nearly impossible.

Motivated, in part, by liquidity concerns during the worst of the financial crisis, China began its effort with a number of bilateral currency swap agreements in 2008 (with South Korea, Malaysia, Belarus, Indonesia, Argentina, Iceland, and Singapore), more recently adding similar agreements with Hong Kong (January 2009) and New Zealand and Uzbekistan (April 2011). These swaps are now valued at RMB829.2 billion (about $127 billion). China is also reportedly discussing the use of local currencies (RMB, ruble, real) to settle trade with Brazil and Russia.

In July 2009, China piloted an RMB trade-settlement scheme.7 By the end of 2010, it had licensed more than 67,000 exporters in 20 provinces to invoice in RMB. Though further expansion is likely, concerns about inflation (mainly caused by China’s excessive, stimulus-related credit expansion in 2009 and 2010) have put efforts on hold, as authorities worry that invoicing in RMB could create additional liquidity,8 China is now focusing on encouraging importers to pay with RMB instead. Once domestic monetary stability is reestablished, China should be able to promote use of the RMB for both purposes.

As for offshore RMB markets, China has made considerable progress in Hong Kong, where residents were first permitted to open limited RMB accounts in 2004—well before the financial crisis. The amounts involved remained small until 2010, however, when deposits surged by almost 400 percent as RMB internationalization intensified.9

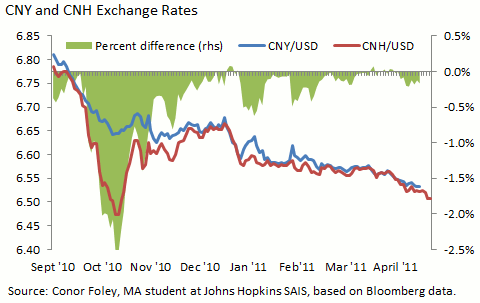

These deposits underpin Hong Kong’s primary market for RMB-denominated financial instruments. The market has expanded rapidly since 2009, when China’s Ministry of Finance issued a small amount of RMB-denominated bonds to promote the market. Since then, several large foreign companies such as HSBC, McDonald’s, and Caterpillar have also issued so-called ‘Dimsum’ bonds. The first RMB-denominated initial public share offering (IPO) took place in April 2011. A secondary market for RMB-denominated securities has yet to develop, however. Because of China’s complex regulations to keep onshore and offshore RMB markets separate and to restrict cross-border arbitrage, interest rates and the dollar exchange rates can and do diverge in the two markets, if only a little (see chart). The arrangements are reminiscent of China’s deliberate “dual-track” approach to domestic market reforms in the 1980s and early 1990s, though today’s arrangements may be maintained for a longer time.

The People’s Bank of China is currently negotiating with Singapore to create a second hub for offshore RMB trading; Kuala Lumpur, Jakarta, Manila, Seoul (and eventually perhaps even Taipei) may be in line as well. Outside Asia, the RMB is hardly traded, but that may change in the years ahead. In January 2011, the Bank of China (China’s third largest bank) began offering limited RMB deposit services in London, New York, and Canada.10

China announced significant additional initiatives for RMB internationalization in January of this year. Chinese firms are now permitted to transfer RMB offshore for investment abroad, with Chinese banks allowed to extend RMB loans for that purpose. Any profits from such investments can be repatriated in RMB. In addition, residents of Wenzhou, a prosperous, entrepreneurial city on China’s east coast, can now directly invest up to RMB200 million (about $30 million at the current exchange rate) per year overseas. Shanghai’s municipal government has reportedly requested similar privileges for its residents.

Long-Term Outlook

In spite of its proactive efforts to promote RMB internationalization, China may not approve all of the measures necessary to achieve full convertibility any time soon. Most significantly, full convertibility would require Beijing to remove its capital account restrictions and many domestic financial controls—measures it relies on for a variety of economic and political purposes, including maintaining a repressed financial system and an undervalued exchange rate.

If its leaders decide to open the capital account, China would have to integrate its capital markets into world markets, with major implications for its state-owned banking system and privileged lending to state enterprises. It would also have to choose between a managed exchange rate and monetary autonomy, as the two are only possible together when capital controls are in place. In addition, China would have to develop the capacity to conduct monetary policy in ways that resemble those of other large economies.11 These changes would have to occur more or less simultaneously.

China’s obvious progress in promoting the RMB as an international currency despite macroeconomic constraints and its apparent unwillingness to commit to full convertibility can be explained by the widespread expectations of rapid growth in China and of further RMB appreciation against the dollar. China’s large and growing presence in the global economy and widespread concerns about the soundness of U.S. macroeconomic policies add to the impetus towards RMB internationalization.

Even if China stops short of full convertibility, the RMB can gain a limited reserve currency role. In fact, Malaysia and some smaller countries in the region have already announced that they have, or plan to, invest a portion of their foreign exchange reserves in RMB-denominated financial instruments. This may be done, in part, for political reasons; whether such decisions are based on ad-hoc convertibility agreements with China is unclear.

This very limited reserve role is a good first step, but the world should more fully embrace the RMB as a reserve currency. An international monetary system based on multiple currencies—with the RMB joining the dollar and the euro as the third major reserve currency—offers a natural extension of the current monetary system and has the potential to alleviate present currency tensions while promoting system stability.

Turning the RMB into a fully convertible international currency would also be good for China. It would, for example, require ending domestic financial repression. This would help China rebalance its economy, give its central bank greater independence, and win recognition as a real “market economy.” It is neither possible nor prudent to make the RMB fully convertible overnight, but the objective should be clear and an approximate timetable would help all concerned.

Footnotes:

1. Many currencies are fully convertible, but only a few also serve as reserve currencies. The four main reserve currencies, in order of current importance, are the dollar, euro, yen, and pound sterling. The decision to use a currency as a reserve currency is to a considerable degree market-determined since central banks want to hold reserves in currencies that are widely used in international transactions.

2. A proposal to make capital account convertibility a required target for all IMF member countries (pushed by the U.S. Treasury) was on the agenda for the IMF’s annual meeting in September 1997. However, as the Asian financial crisis had begun just a few months earlier, the proposal gained no traction, as members worried about how an open capital account would affect economies with under-developed financial institutions, including China. In contrast to the 1997 proposal, this March, the IMF came out in support of limited capital controls under certain circumstances.

3. The book asserts that the Rothschild banking dynasty has had a pervasive influence on world history over the last few centuries and that even the Federal Reserve is ultimately controlled by private banks owing allegiance to the Rothschilds. Fortunately, well-trained economists in China’s central bank recognize this convoluted conspiracy theory for what it is, but that does not mean they can ignore public opinion. This is bad news for those interested in improving stability in the international monetary system, which requires China’s active involvement and cooperation.

4. Zhou Xiaochuan, governor of the People’s Bank of China, made another proposal for decreasing reliance on the dollar in 2009. He suggested converting the IMF’s Special Drawing Right (SDR)—a basket of four currencies, the US dollar, euro, yen, and pound sterling—into a broad-based international currency, usable not only as a reserve asset, but also for trade settlement and corporate accounting around the world. Although the proposal had no chance of practical implementation—the United States has de-facto veto power and no incentive to reduce the international role of the dollar—it was well received by many developing countries and in Europe. Since then, China has made no effort to revive its proposal—Beijing’s attention is now focused on RMB internationalization. However, Brazil has taken up the baton by calling for international financial system reform in various international forums.

5. HSBC analysts estimate that, prior to the crisis, some 70 percent of China’s exports and imports was invoiced and settled in U.S. dollars and the rest mostly in euros and yen.

6. Of the nearly $200 billion in foreign exchange reserves that China accumulated during the first quarter of 2011, about 25 percent was due to China using more RMB to pay for imports than to invoice exports. Over that period, about 13 percent of China’s imports (including most imports from Hong Kong) were paid for in RMB, while less than 2 percent of China’s exports were invoiced in RMB.

7. China reported that the share of its international trade settled in RMB increased to 7 percent in the first quarter of 2011 (from less than 1 percent in the first quarter of 2010).

8. Another factor slowing export invoicing in RMB is that it is reportedly much harder to claim Value-Added Tax export rebates when exports are invoiced in local currency.

9. Deposits reached RMB 408 billion ($62 billion) in February 2011. While this is still a relatively small amount, the rate of growth is astonishing. At the end of March 2011 RMB deposits accounted for 14 percent of non-Hong-Kong-dollar deposits in Hong Kong up from about 1 percent at the beginning of 2010, mainly at the expense of U.S. dollar deposits. Chinese payments for imports account for the bulk of these deposits, but personal RMB transfers from mainland China—presently capped at RMB20,000 (a little over $3,000) per day and generally coming from visitors and tourists—are also important.

10. The New York branch of Bank of China began accepting up to $4,000 per day (up to a maximum of $20,000 per year) in RMB deposits for individual clients and higher amounts for corporate accounts.

11. For monetary policy, China still relies heavily on direct deposit and lending rate controls as well as quantitative lending targets. Once its domestic capital markets are more fully developed and integrated into global markets, indirect controls, such as the Federal Reserve’s federal funds rate, will have to move center-stage.

Uri Dadush, author of the book Juggernaut, is the director of Carnegie’s International Economics Program. Pieter Bottelier, former chief of the World Bank’s resident mission in Beijing, is a nonresident scholar in Carnegie’s International Economics Program and senior adjunct professor of China Studies at the School of Advanced International Studies (SAIS) at Johns Hopkins University.

Không có nhận xét nào:

Đăng nhận xét